Luminance

Tools

After Effects, Blender, Figma, Photoshop, and Protopie.

Team

Thayna Santana, Larry Tian and Veneza Yuzon.

My Role

User Research, User Experience Designer, 3D Designer, and Motion Designer.

Duration

6 Months.

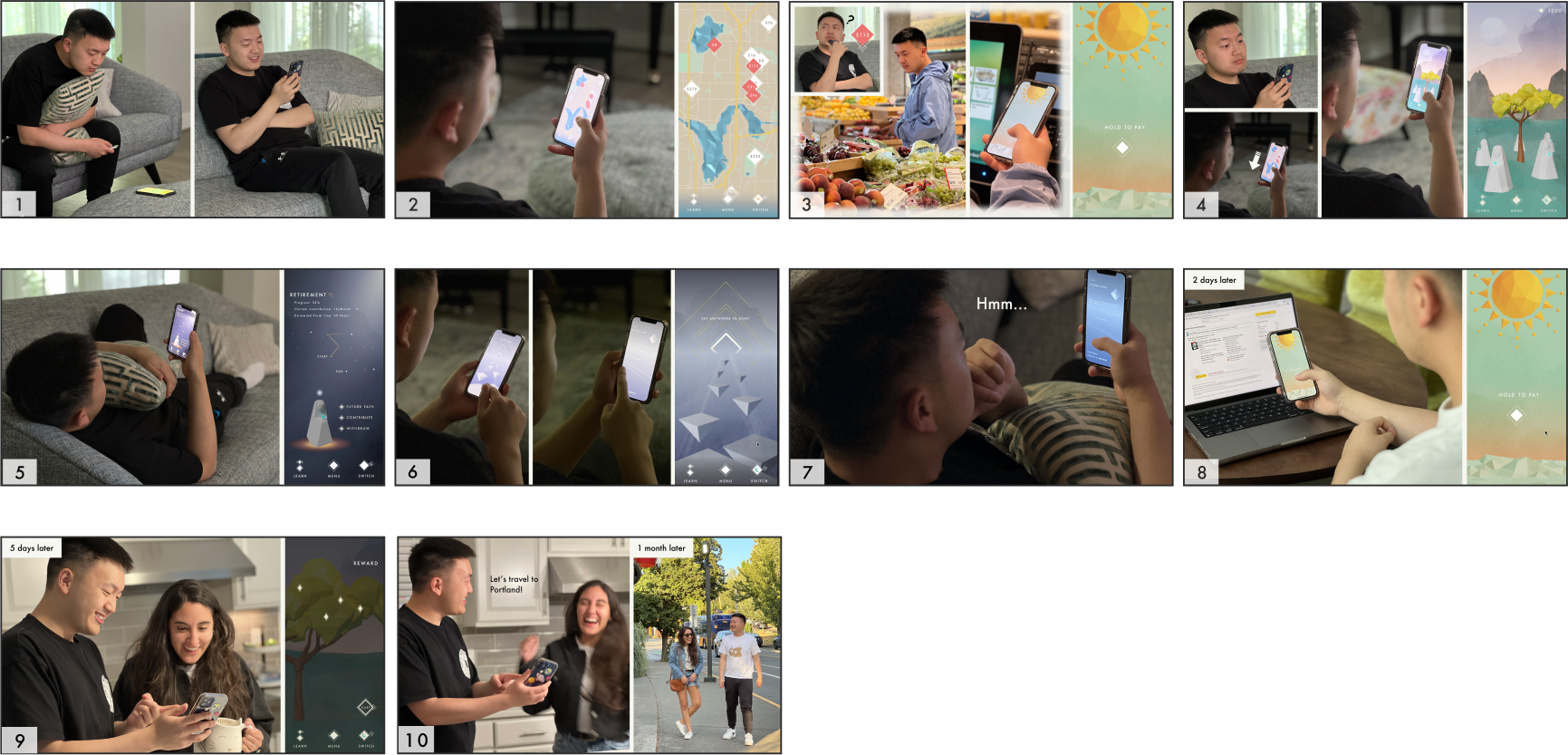

In this video, meet Yolanda, a vibrant young adult striving to cultivate healthier financial habits. She's determined to secure a stable future while savoring the present, making meaningful purchases that bring joy and fulfillment to her life.

Shortcut

Overview

Luminance acts as a financial management catalyst, helping young adults envision their financial future by enhancing savings motivation and infusing a sense of purpose into their financial goals.

It encourages users to go beyond the routine of spending and financial transactions, fostering a reflective approach. Users become highly conscious of how their financial decisions impact their progress toward future goals without sacrificing their present quality of life.

-

Users can track their financial journey, measure their milestones, and adjust their course as needed, creating a dynamic and evolving approach to their financial well-being. In essence, Luminance transforms financial management into a journey of self-discovery, motivation, and continuous progress.

Key Interactions

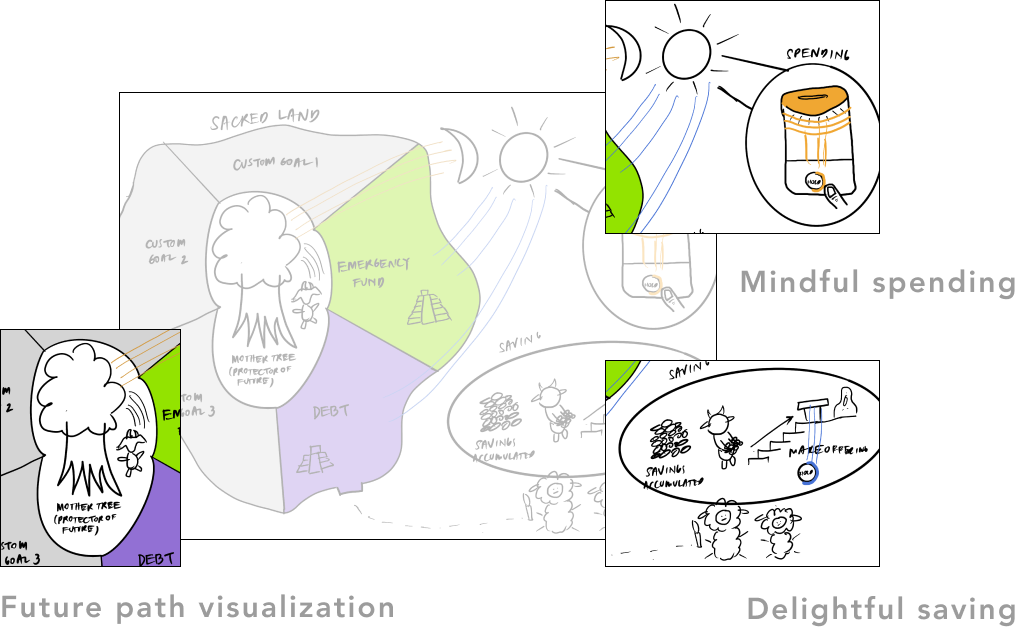

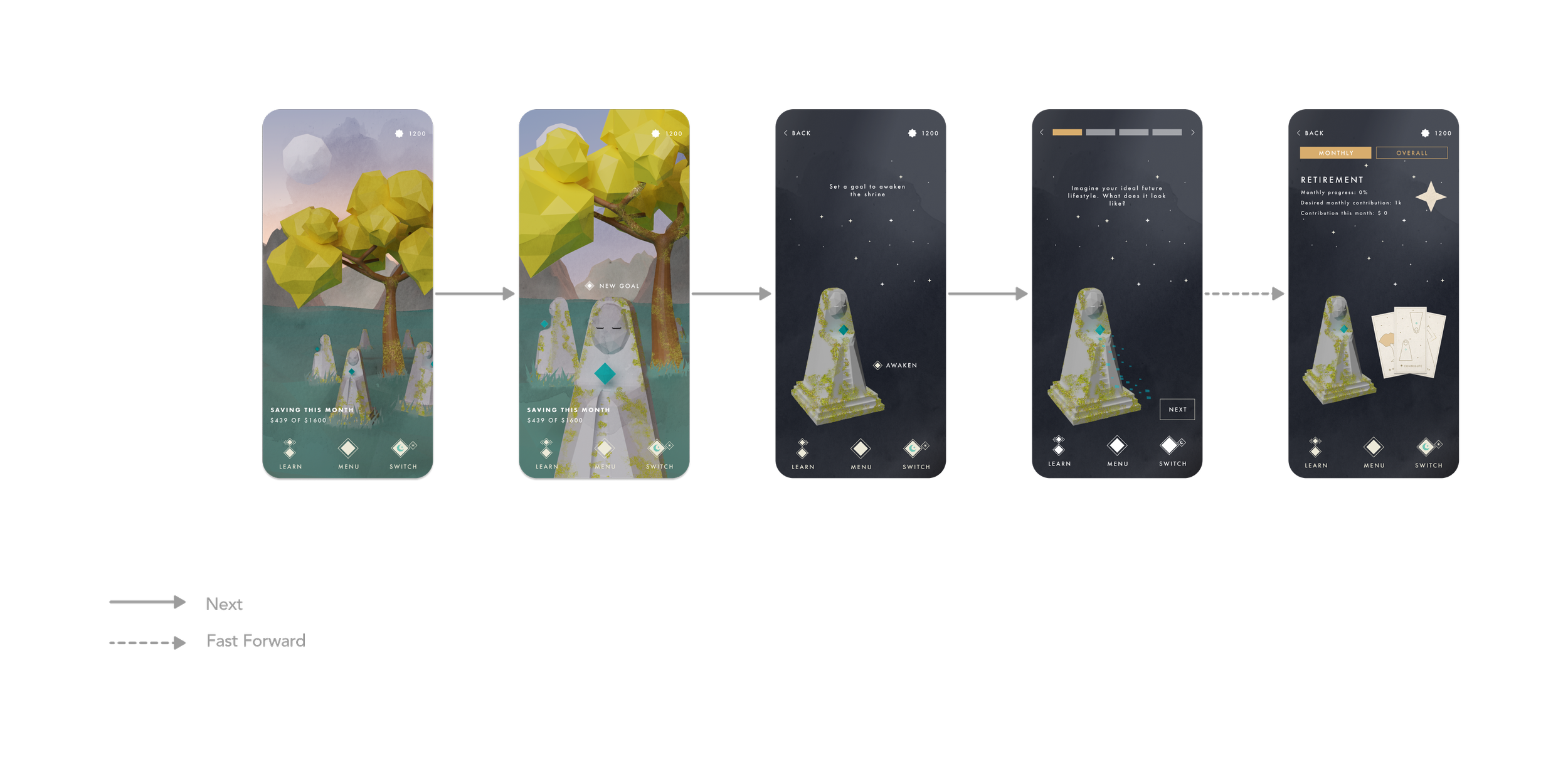

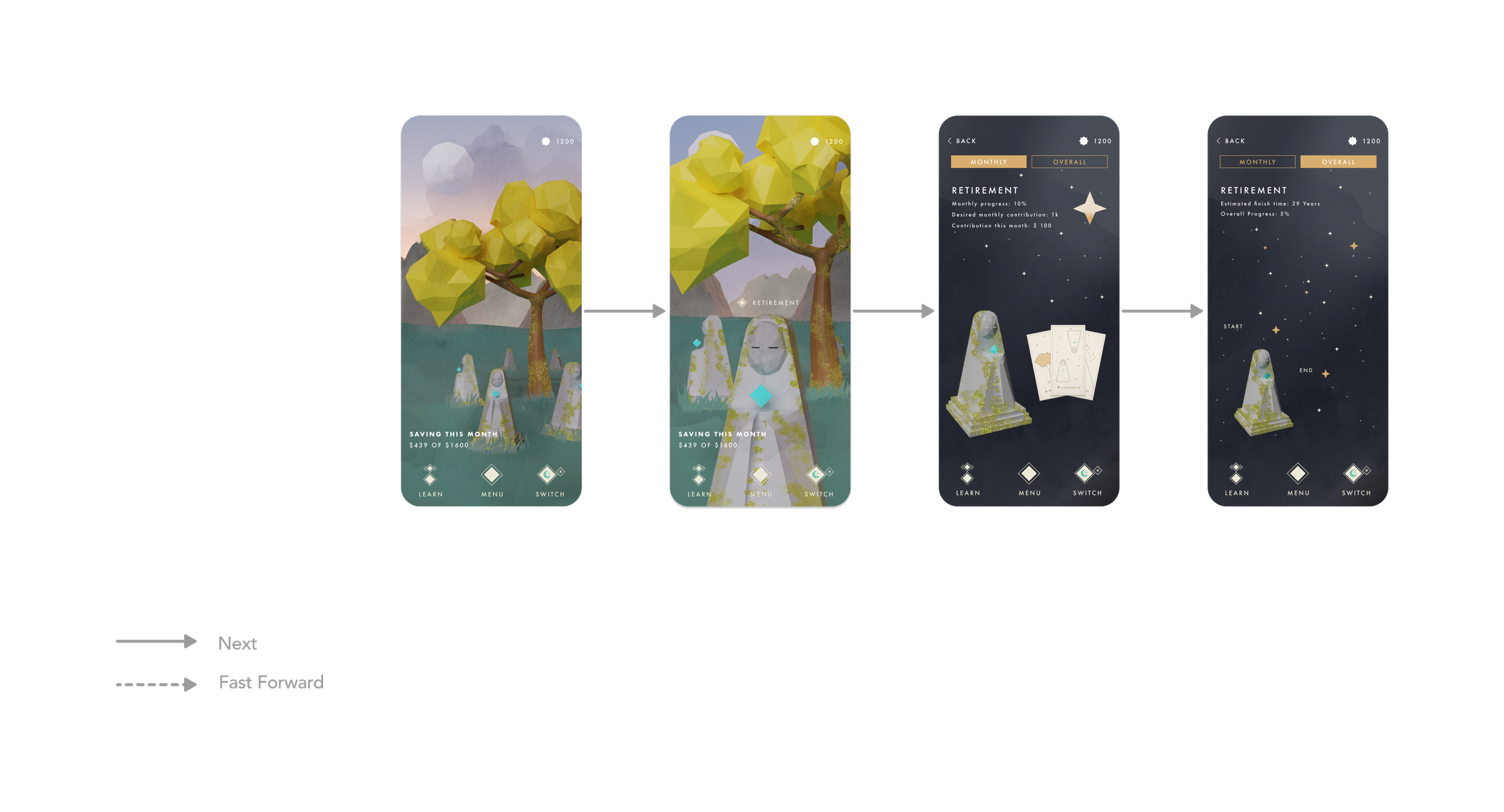

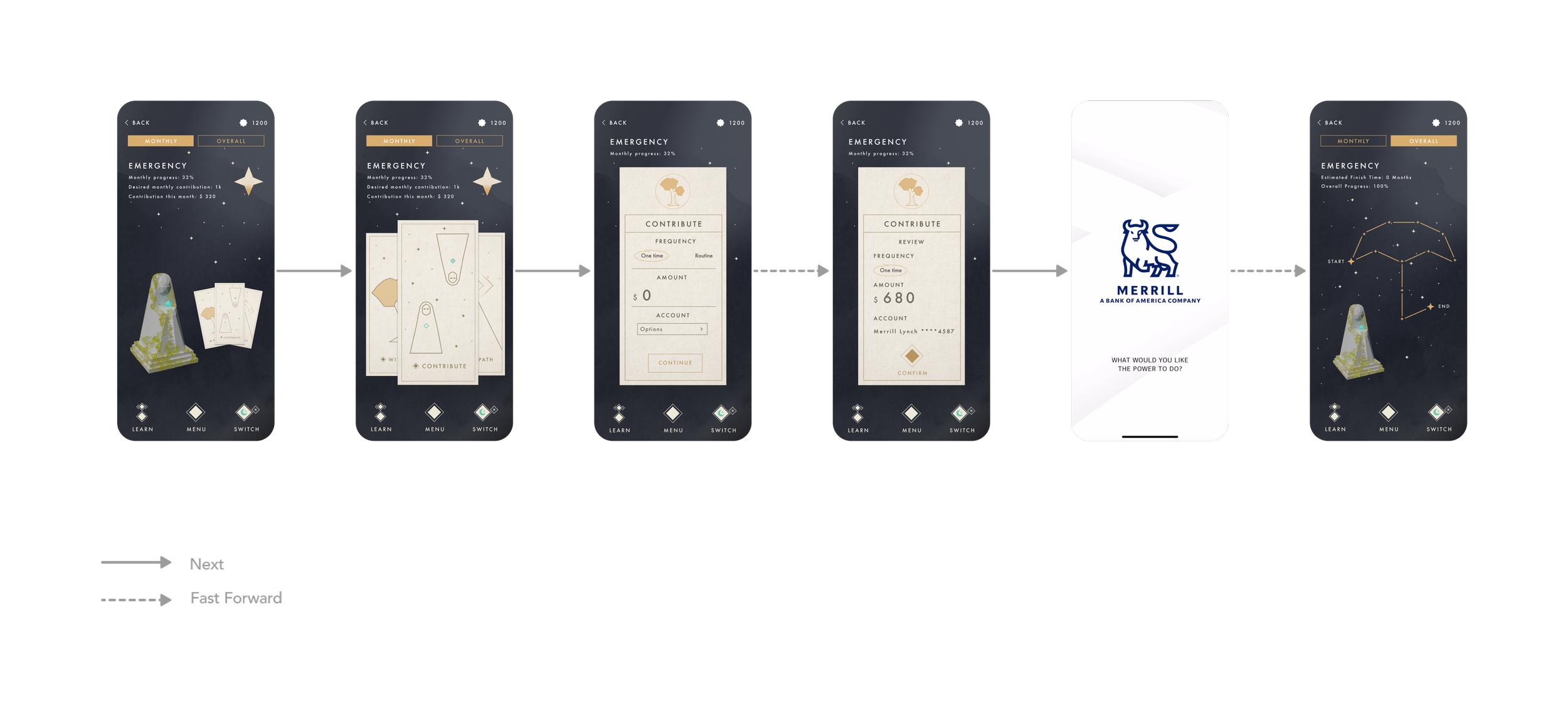

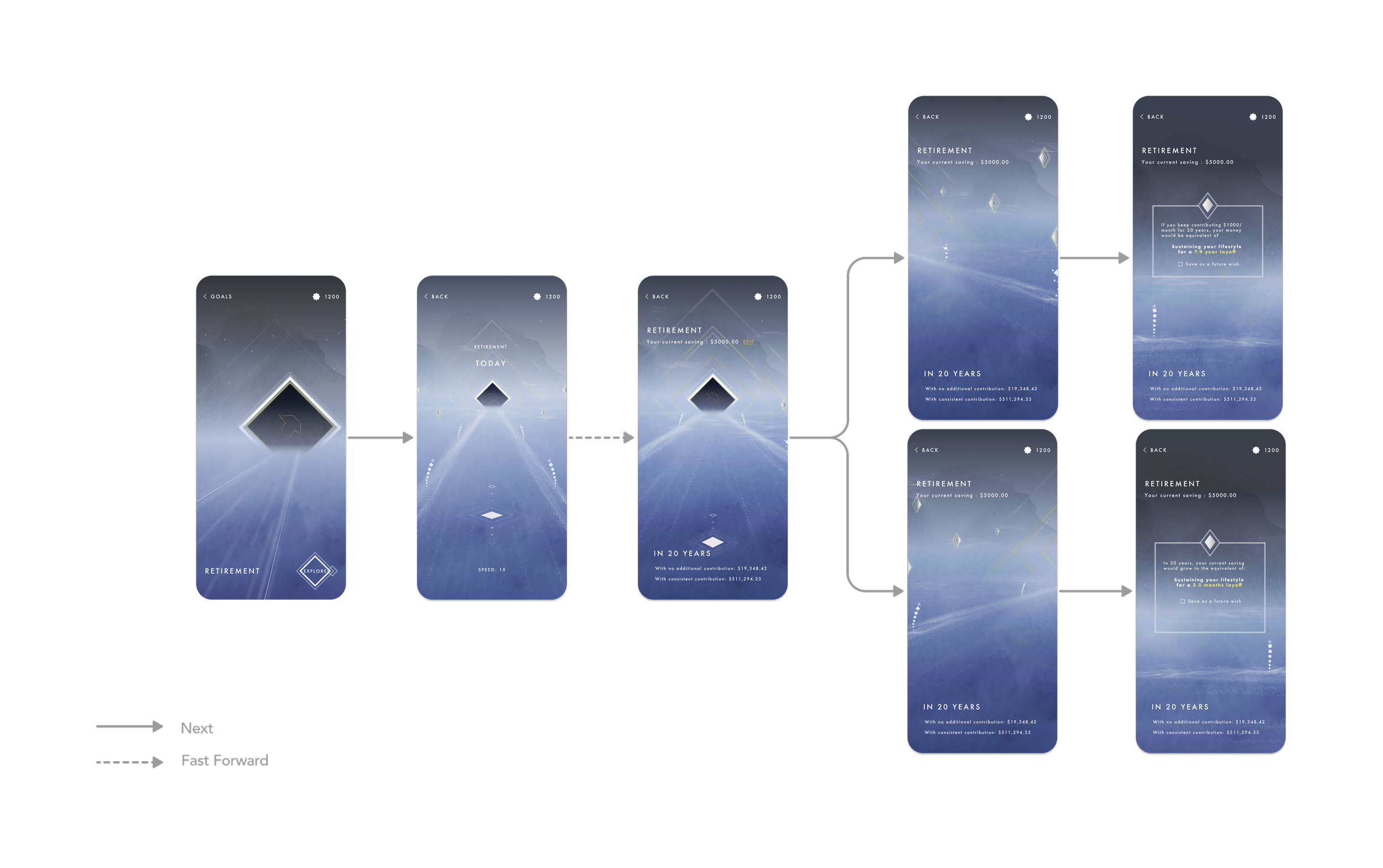

Simplifies Future Planning for young adults, emphasizing the importance of goal setting and contribution to their plans without sacrificing the present, and allows them to track their progress using user-drawn icons representing their goals

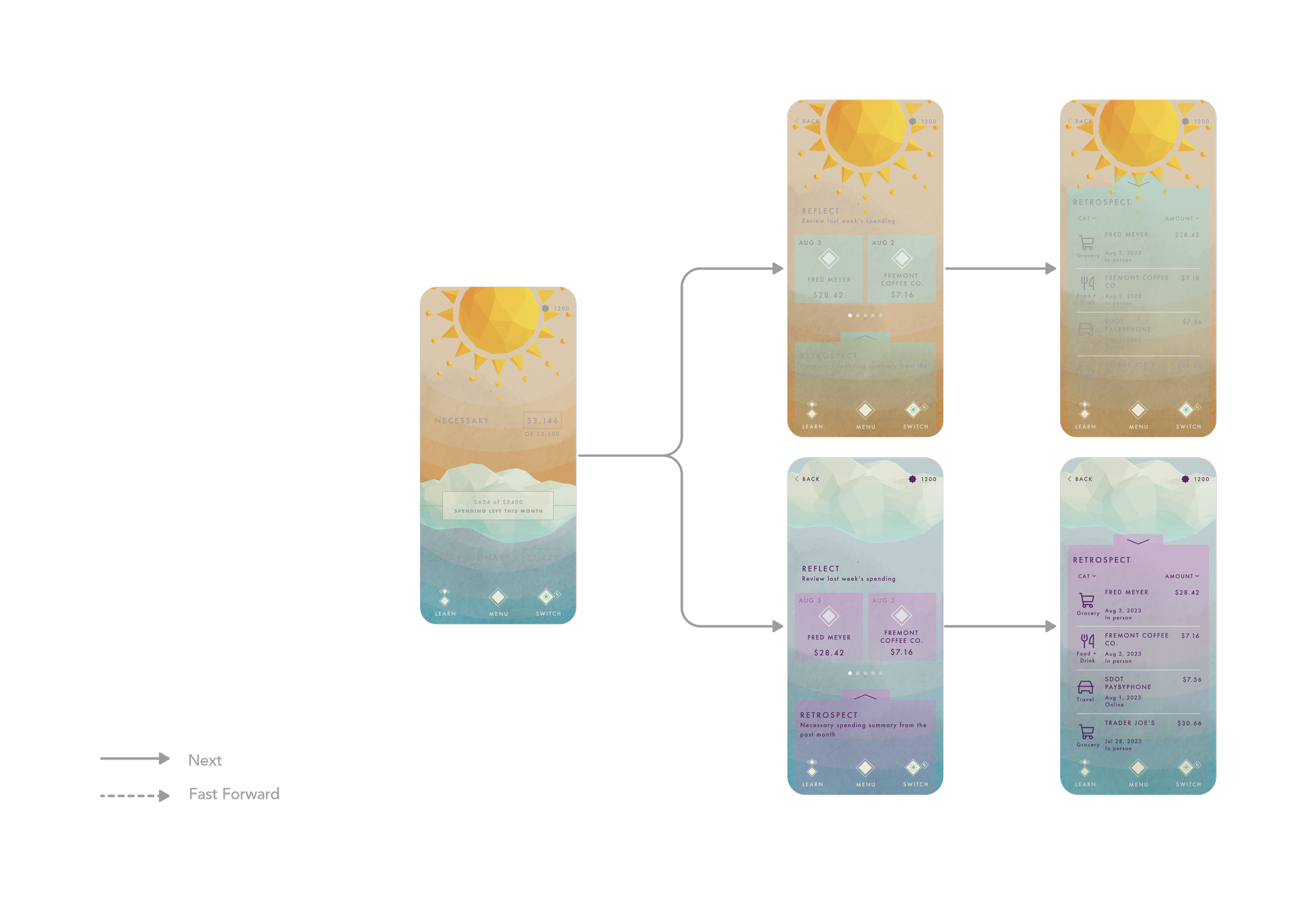

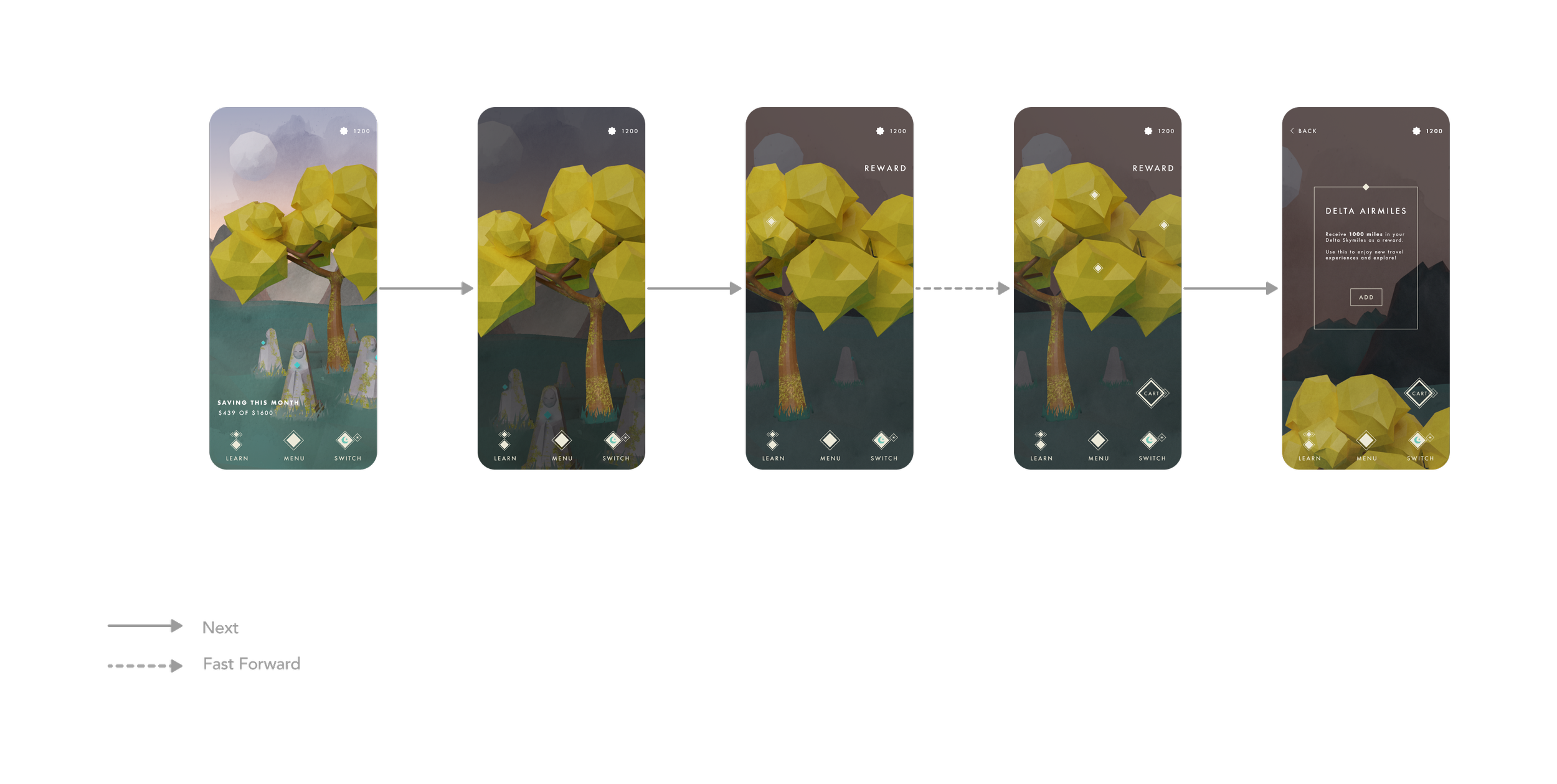

Promotes Mindful Spending by prompting young adults to reflect on their expenses before and after, fostering comprehensive financial awareness.

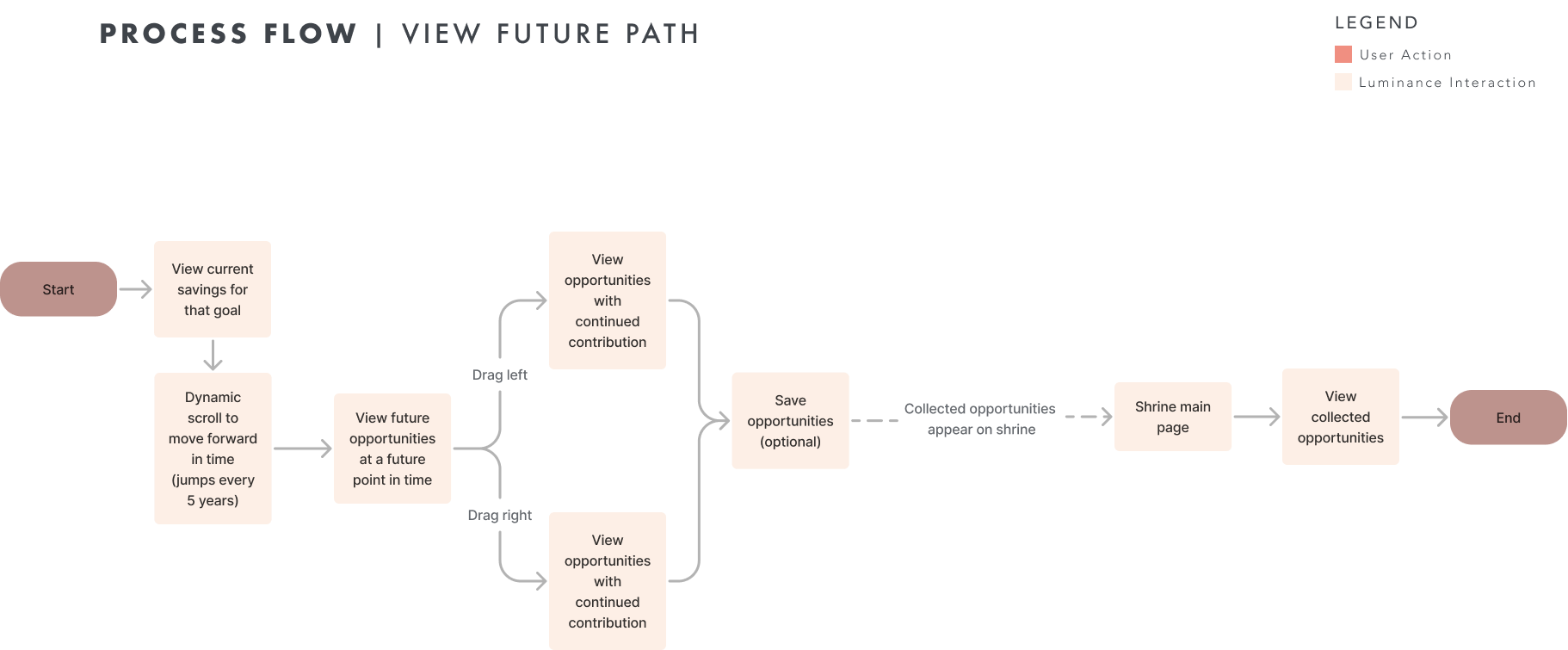

The unique "Future Path" feature lets young adults visualize savings growth and explore different saving opportunities represented as stars, making future planning personalized and enjoyable.

Situation

27% of American households reach retirement age with minimal or no savings, necessitating continued employment to cover their living expenses, including the escalating costs of healthcare. (Source)

The financial future of many young adults, particularly those aged under 29, often takes a back seat in their priorities. In fact, an alarming 66.2%, mainly among Millennials, found themselves without any retirement savings during this period. This shortfall in savings can be attributed, in part, to the allure of materialism and the desire for immediate gratification, which frequently lead to impulsive financial choices.

-

Users can track their financial journey, Furthermore, many young adults view retirement as a distant, abstract concept, further postponing any preparations. A lack of financial knowledge and understanding of retirement options compounds the issue, discouraging them from setting funds aside. Early exposure to financial education has the potential to significantly reshape the financial behaviors and overall well-being of young adults, alleviating stress in financial matters such as budgeting, bill payment, borrowing, and investing. It's worth noting that while young adults, in general, tend to save less for retirement, married couples show a greater propensity for retirement savings compared to their single counterparts.

Research

In our study, we confirmed that young adults lack the motivation to save for retirement due to uncertainty about the future. Stable income is crucial before they consider saving. Our research showed that young adults prioritize experiences and joy in their spending and saving choices, which affects how they view retirement planning. We also found a significant difference in how they see emergency saving compared to retirement saving. Additionally, we gained insights from financial advisors, giving us a comprehensive understanding of the problem. These findings will guide our future design decisions.

-

We conducted a comprehensive research effort, interviewing a total of 10 young adults. Five of them participated in the probe, providing valuable insights into their real-time financial behaviors, while the remaining five engaged in semi-structured interviews, allowing us to gain a deeper understanding of their perceptions and habits related to savings and retirement. This balanced approach provided us with a well-rounded perspective from this demographic.

Our research also included five in-depth semi-structured interviews with Financial Advisors, who served as our subject matter experts. These interviews were instrumental in enhancing our understanding of finance and young adults' financial behaviors. Leveraging their professional insights, we gained valuable perspectives that enriched our project's depth and relevance to the real-world financial landscape.

Participant Profile

Young Adult

Age: 18-29

Rationale: Nearly half of the adults will be financially independent by the age of 29.

Financially independent: People who manage their finances independently, not with someone else

Rationale: Married persons are more likely than their single counterparts to participate in a defined contribution pension plan3.

Income: At least the median range based on their city of residence

Rationale: To better define the range of adults who are able to meet all of their basic needs but don’t feel like they have extra money to save, we are using the median income of their respective city of residence as a baseline.

Gender: Diverse

Rationale: We’d like to get a more diverse range of perspectives.

Location: Diverse (interviews) + Seattle based (probes)

Rationale: We’d like to get a more diverse range of perspectives, so we will recruit people from various parts of the country for remote interviews. However, for the probes, we’d like to recruit local participants based on the logistics of the probe activity.

Education: No full-time students, but otherwise no other criteria

Rationale: Since it is more likely that full-time students would not have income that allows them to self-sustain their cost of living and other finances, we assume that most full-time students are not fully financially independent without some support from student loans or family help. Otherwise, we assume that education should not affect the results as long as participants feel financially secure.

Financial Advisor

No specific criteria. The objective was solely to gain insights into the problem space from a professional perspective.

Methods

Semi-structured interviews Young Adults

In our semi-structured interviews with young adults aged 18-29, our primary goal was to gain deep insights into their perceptions of saving, particularly in the context of retirement and future goals. We aimed to uncover their saving habits and behaviors, shedding light on what actions this demographic had been taking, or perhaps neglecting, concerning retirement planning.

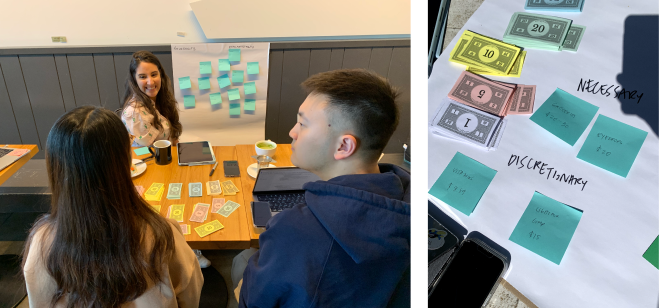

Probe activity Young Adults

The study aimed to understand participants' real-time financial habits by analyzing their expenses, distinguishing between discretionary and necessary spending, and calculating their discretionary expenses. The goal was to assess how these factors influenced their perceptions of saving and future financial behaviors. Participants were also asked to write a letter to their future selves, providing insights and guidance on their financial habits.

Semi-structured interviews SME

The semi-structured interview with financial advisors served the purpose of obtaining professional insights into recommended saving habits for young adults. Furthermore, given financial advisors' expertise in financial management, we sought their perspectives on the factors that motivate young adults to save money. Engaging with financial advisors provided an opportunity to validate certain hypotheses and acquire a more profound comprehension of the problem space from their professional standpoint.

Findings

Need clear vision to see savings value

Young adults need to have a clear vision of their financial goals to see the value in saving.

-

“[About retirement] I don't have like a really concrete sense of my goals and my desires. So it's a lot easier to get myself to do something because someone else wants it or someone else is telling me to do it. As opposed to oh, I want to do it.” - Participant 5

“[About retirement] I don't envision that yet. I am putting money because I know I have to. But, you know, there's a lot of variables that I'm not sure about.” - Participant 8

Use reflection to assess next steps

Once young adults have a goal, they use reflection to help them assess the steps needed to achieve that goal while ensuring they maintain financial stability.

-

“If I know I'm going to travel [...] That's when I really try to take the time and focus on like, do I really need the coffee when like I can make coffee at home because like even the smallest expenses add up in the end.” - Participant 6

“Because saving is ultimately is ultimately a self of form of self-care, you're protecting your future, you're making sure that you're not anxious in the future, you're making sure that you're well cared in case of an emergency.” - Participant 8

Value joy as saving motivator

To motivate young adults to save, it's important to create experiences that bring them joy. Games are a common interest among this demographic, and some even learn about finances through gaming.

-

“They’d like to talk about this ‘financial’ topic with me, but I’d stop them since I think it is kind of boring since the end goal is for me to save more.” - Participant 3

“But now you showed me the compound interest thing maybe I'll cut some joy out of my life and get 300k, but not all the joy of my life.” - Participant 4

“So even when I was young, when I play like virtual games, I would just call it the virtual currency.” - Participant 2

Experiences shape financial behaviors

Experiences (both past and future) influence how young adults justify their financial decisions and behaviors.

-

“Prioritizing spending money on the things that matter most to you, your family traveling community and less on the things that don't or take away from your experience.” - Participant 1

“Out of all the expensive things that I'm I'm uncomfortable with, spending on experiences shared experiences are what I'm most okay with.” - Participant 5

Prioritize security for short term

While young adults have uncertainty about retirement, they do prioritize having a safety net to ensure a sense of security for the immediate future.

-

“I just it's really hard for me to feel I guess the effect on my future if it's so far away. Because I just don't believe in I guess prioritizing my future me as opposed to like present me” - Participant 5

“I personally don't see the point of a 401 K because it's not even a guarantee that I'll be alive by that age.” - Participant 9

Want to pursue their hobbies/ interests

Young adults emphasize an ideal future lifestyle where they can work on their hobbies/ interests.

-

“The concept of like passive income, or owning your own business, or generating your own revenue through your own resources, that I would rather be 65 and just have like, a small business that nets me.” - Participant 9

“I'm one of those people that doesn't think that I won't be able to work not because of making money but just because of the way that I am like if I'm just not doing anything, I kind of go crazy. So I would love to spend my retirement just like doing things that I enjoy.” - Participant 2

Objective

Increase financial literacy and awareness among young adults, helping them understand the importance of financial planning and retirement savings

Encourage young adults to adopt more mindful spending habits by making them aware of the consequences of their financial choices

Create an engaging and user-friendly experience that makes financial planning and saving an enjoyable and personalized journey for young adults

Design Principles

-

Interesting and engaging so users are willing to use it.

-

Help users to reflect in order to learn.

-

Provide people a sense of security to both take risks and protect their future.

-

Make information specific to the user’s situation and needs.

-

Ensure people are informed without being overwhelmed by taking a step-by-step approach, in order to maintain balance in their life where they can enjoy their youth while still proactively saving for their future.

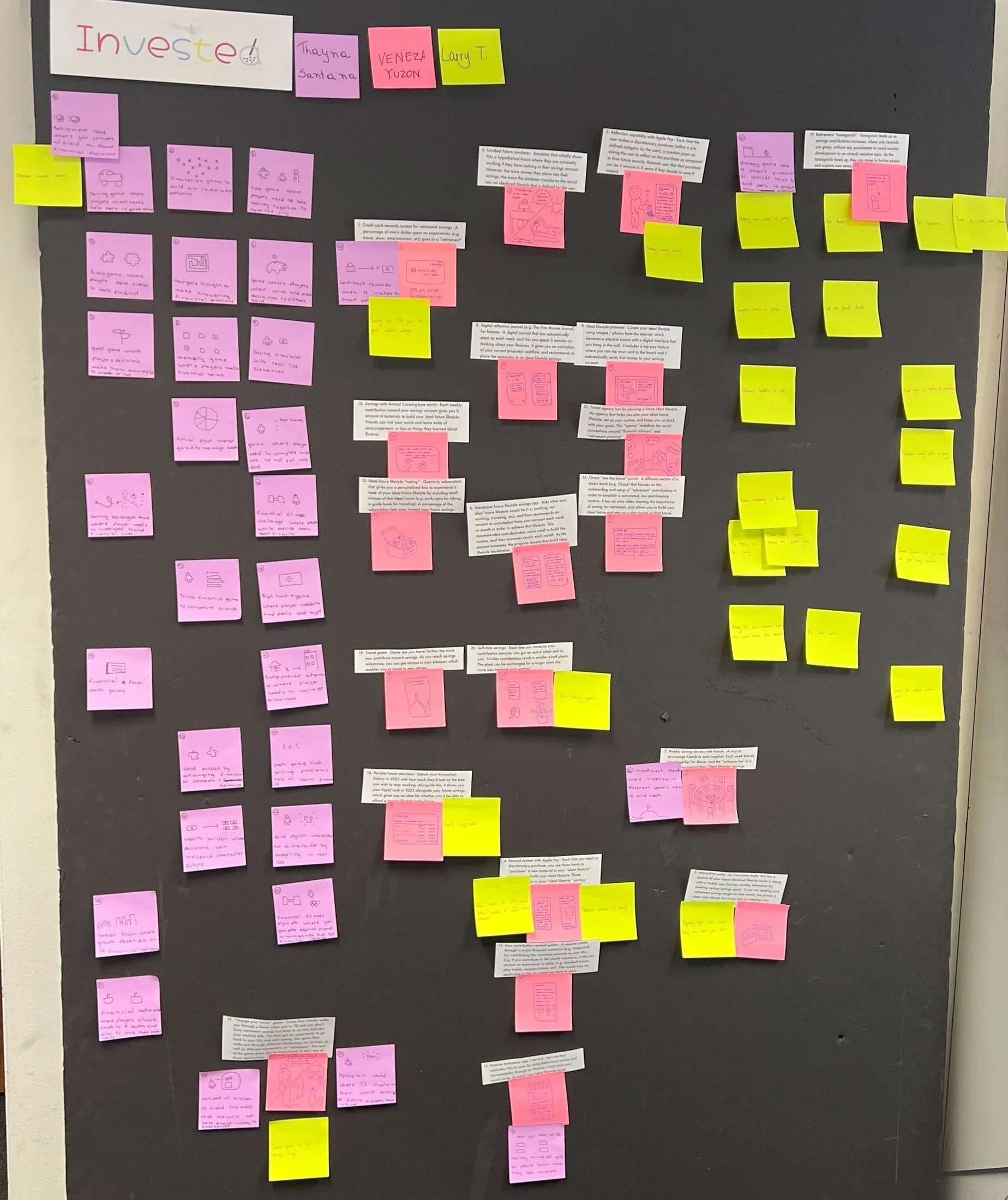

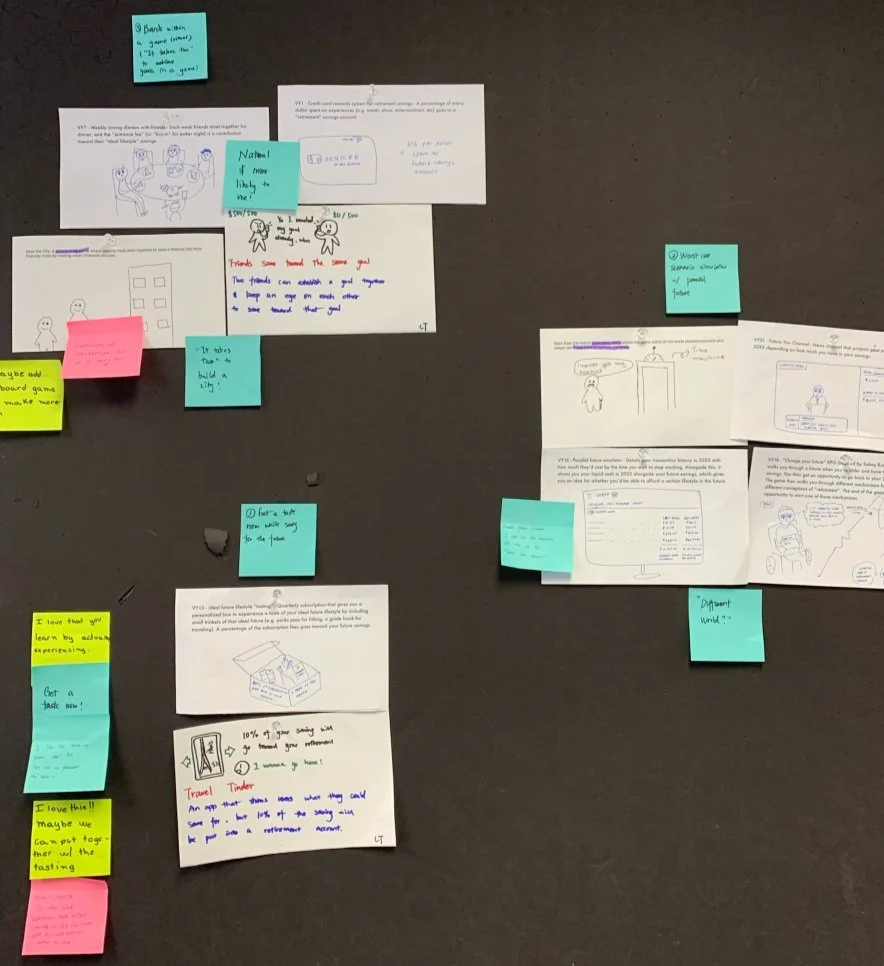

Ideation

During the ideation phase, we followed a meticulous process to narrow down our ideas and identify the most promising directions. Initially, we applied key design principles and desired outcomes as our guiding criteria. We then employed dot-voting to gauge the collective enthusiasm for each concept. Subsequently, we scrutinized the ideas through the lens of our research findings, eliminating those that didn't align with our insights.

As a team, we engaged in a brainstorming session that generated a total of 79 ideas. These ideas revolved around various themes, including visualizing worst-case scenarios, gamification, rewards, rethinking banking, enhancing services, connecting finance with fitness, collectibles, and simulations, among others.

To further refine our selections, we organized the remaining ideas into categories, allowing us to assess their collective strengths and weaknesses. This categorization helped us pinpoint what we liked and disliked about each group, facilitating more informed decisions. Finally, we conducted a personal interest assessment to ensure that the chosen concepts resonated with the team's passion and vision, ultimately leading us to the most promising ideas for further development.

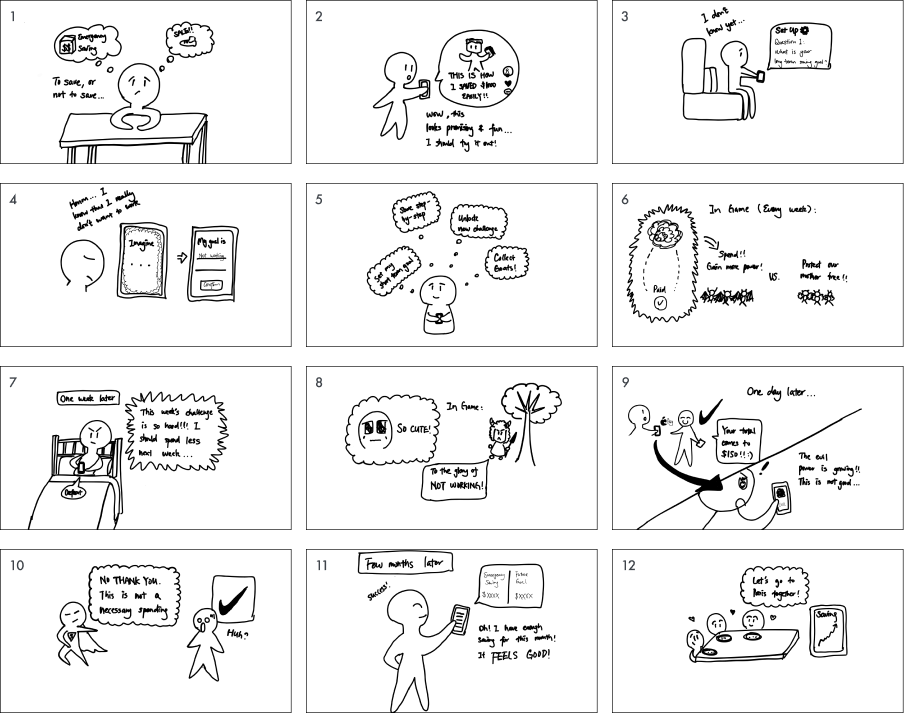

Initial Storyboard

During the initial storyboard process, our team embarked on a mission to ensure everyone had a shared understanding of the product and its vital functionalities. This phase was characterized by our enthusiasm for creating an engaging, gamified experience, temporarily setting aside the financial aspects to prioritize the fun factor.

After receiving valuable stakeholder feedback, we had a significant revelation that our initial approach of gamifying without a clear purpose didn't align with our goals. In response, we made a strategic decision to pivot and returned to the ideation phase, committed to finding innovative solutions that went beyond superficial gamification. This shift marked a pivotal moment, propelling us to dive deeper into the creative process, seeking more holistic and impactful ways to enhance our project's value and purpose.

Refined Storyboard

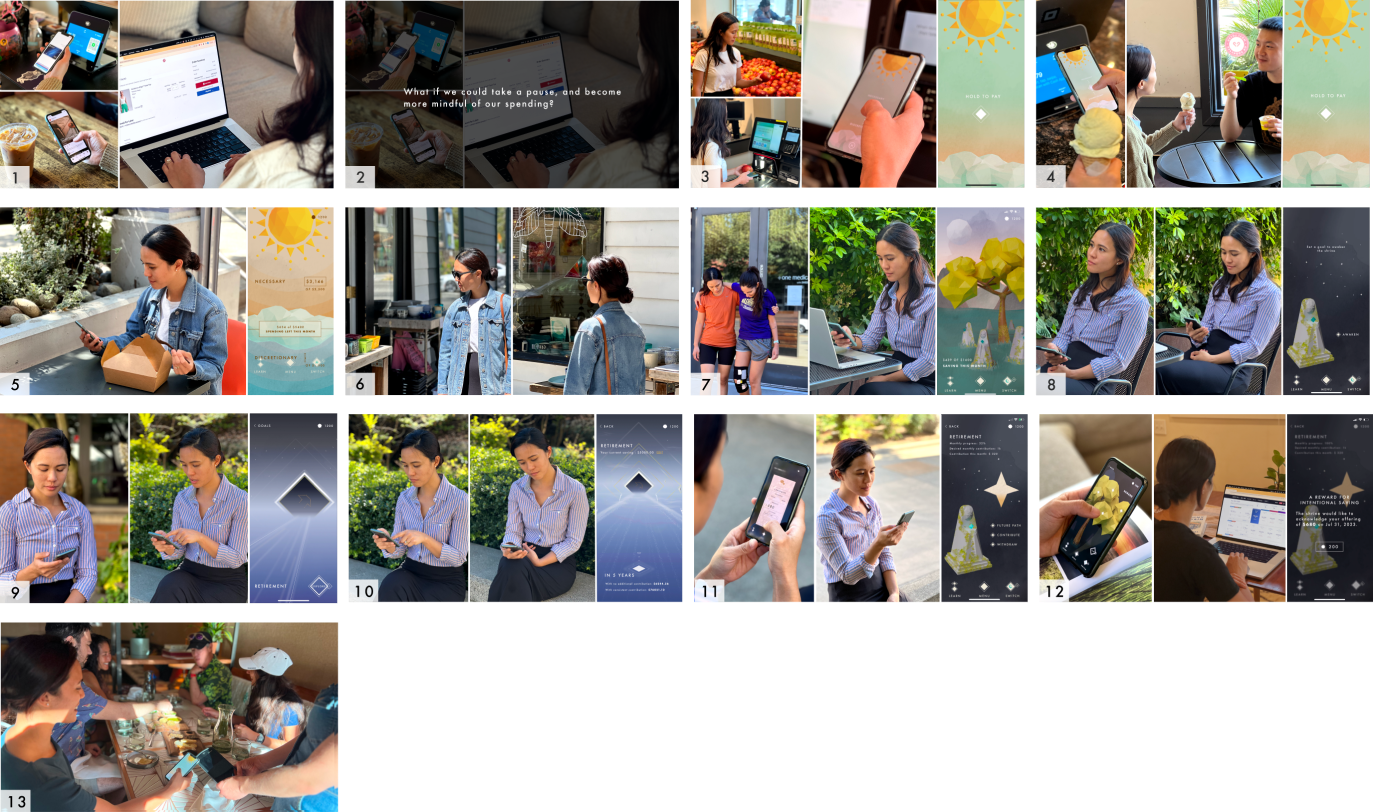

The second version of the storyboard received positive feedback, but the team decided to refine it by introducing more variety in the main character's surroundings. Instead of a seated position, scenes were filmed in different locations, enhancing the viewer's experience and creating a more relatable and visually captivating narrative.

The refined storyboard became the project's guiding blueprint, seamlessly integrating gamification elements with crucial financial management features to provide a well-defined narrative structure. This creative journey infused our project with a clear sense of purpose, significantly enhancing its overall value and impact.

Following feedback on the initial refined storyboard, we recognized that the main character appeared overly sedentary, resembling a couch potato. In response, we made revisions to the second version.

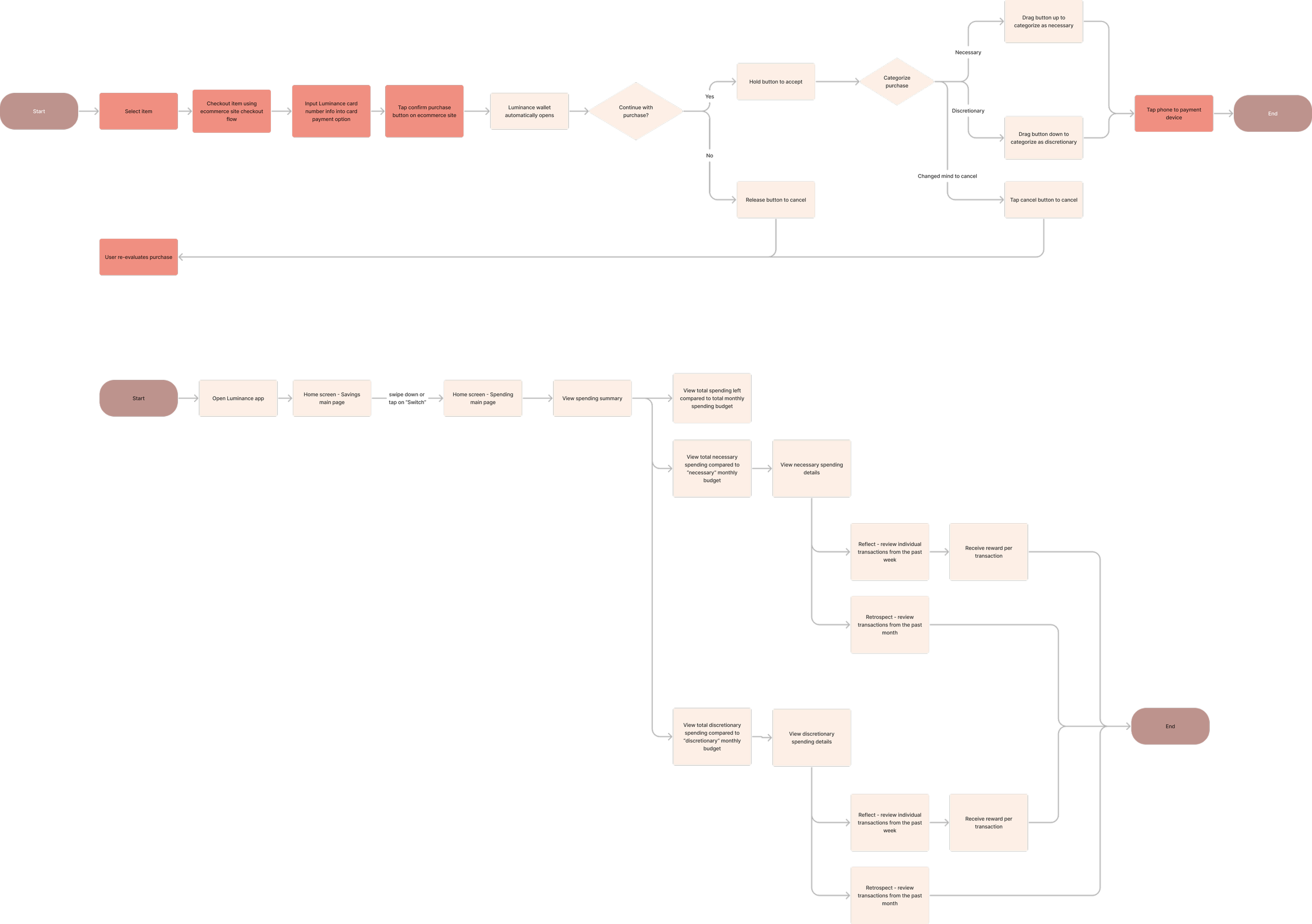

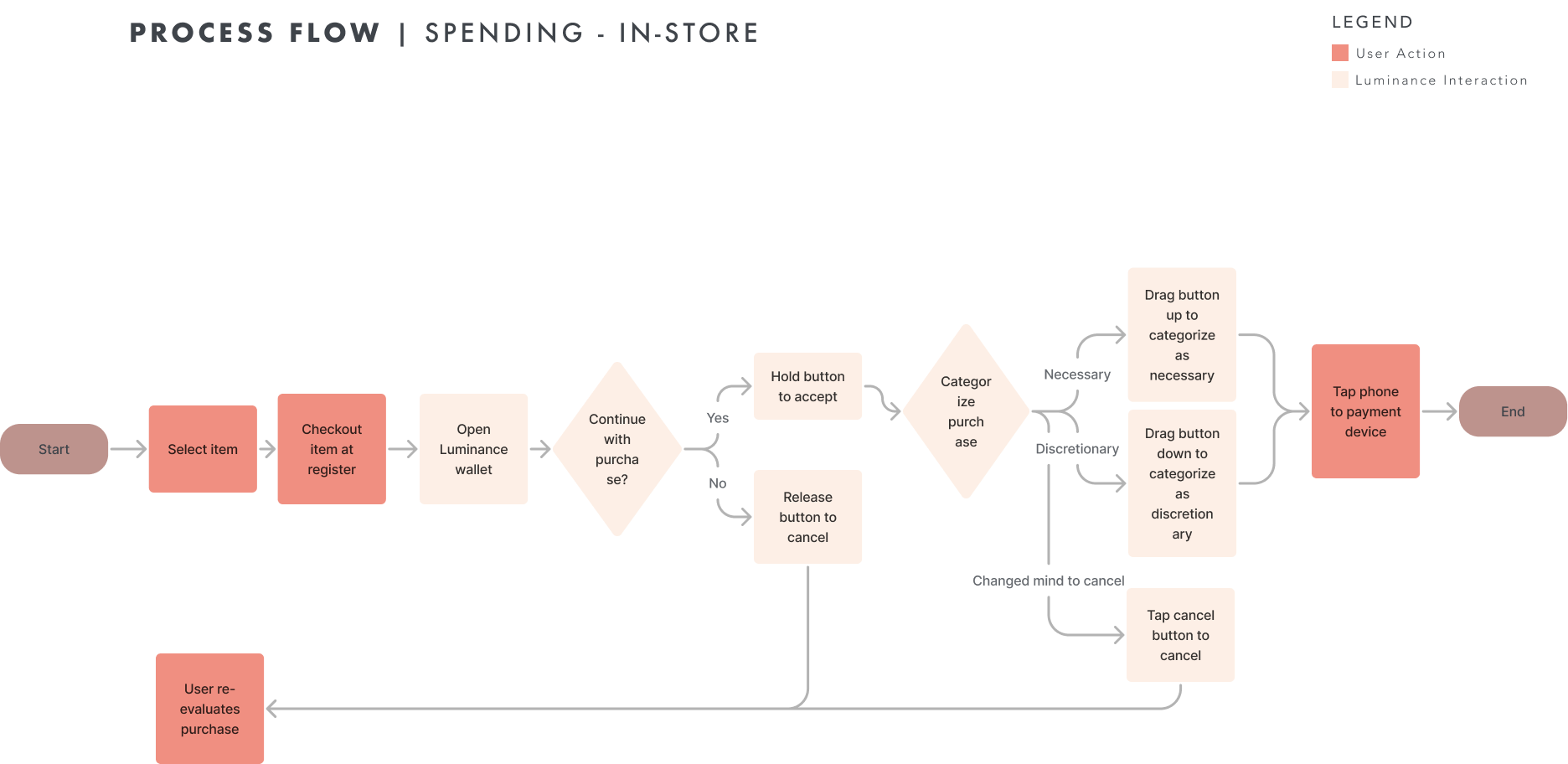

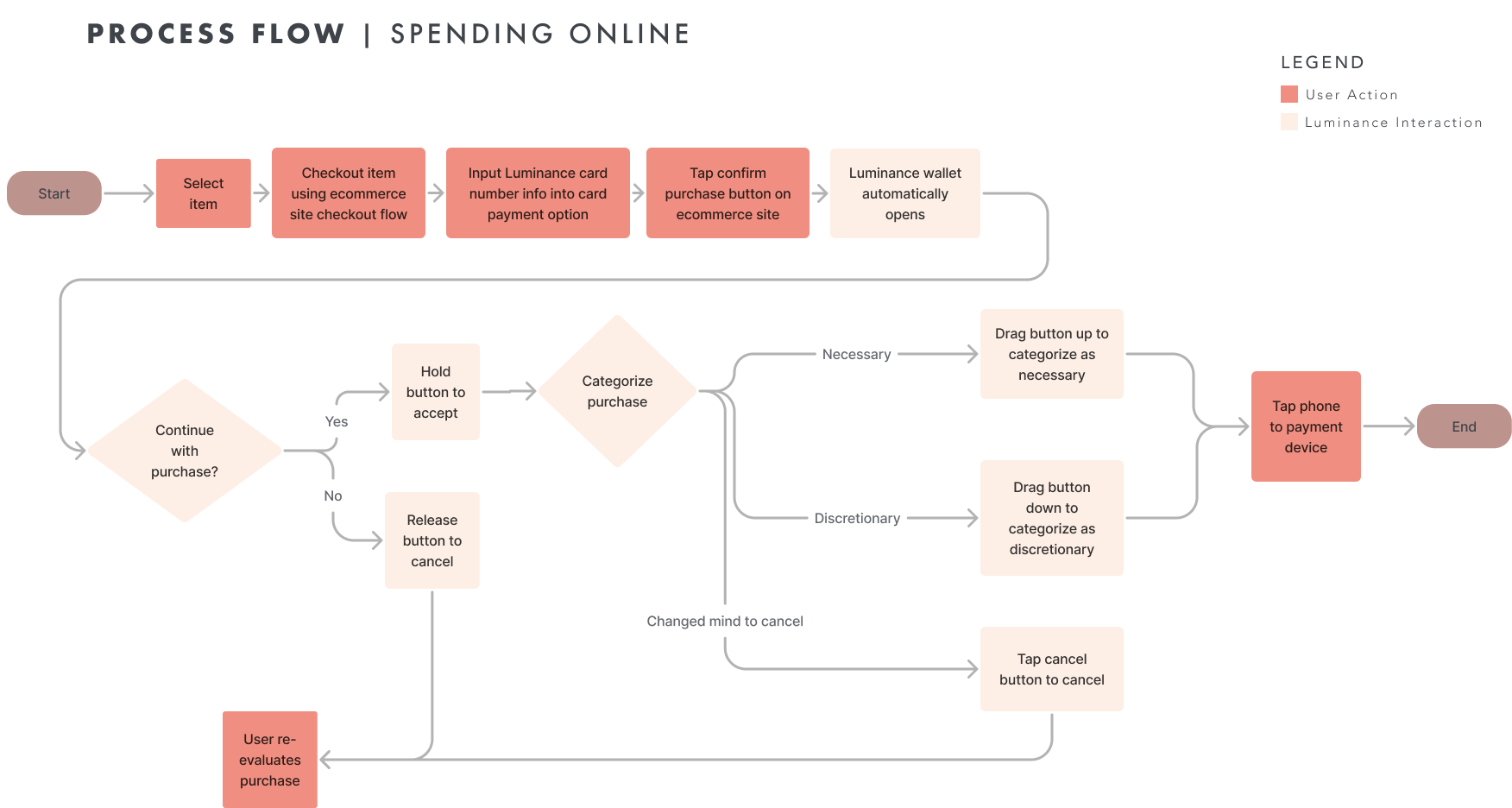

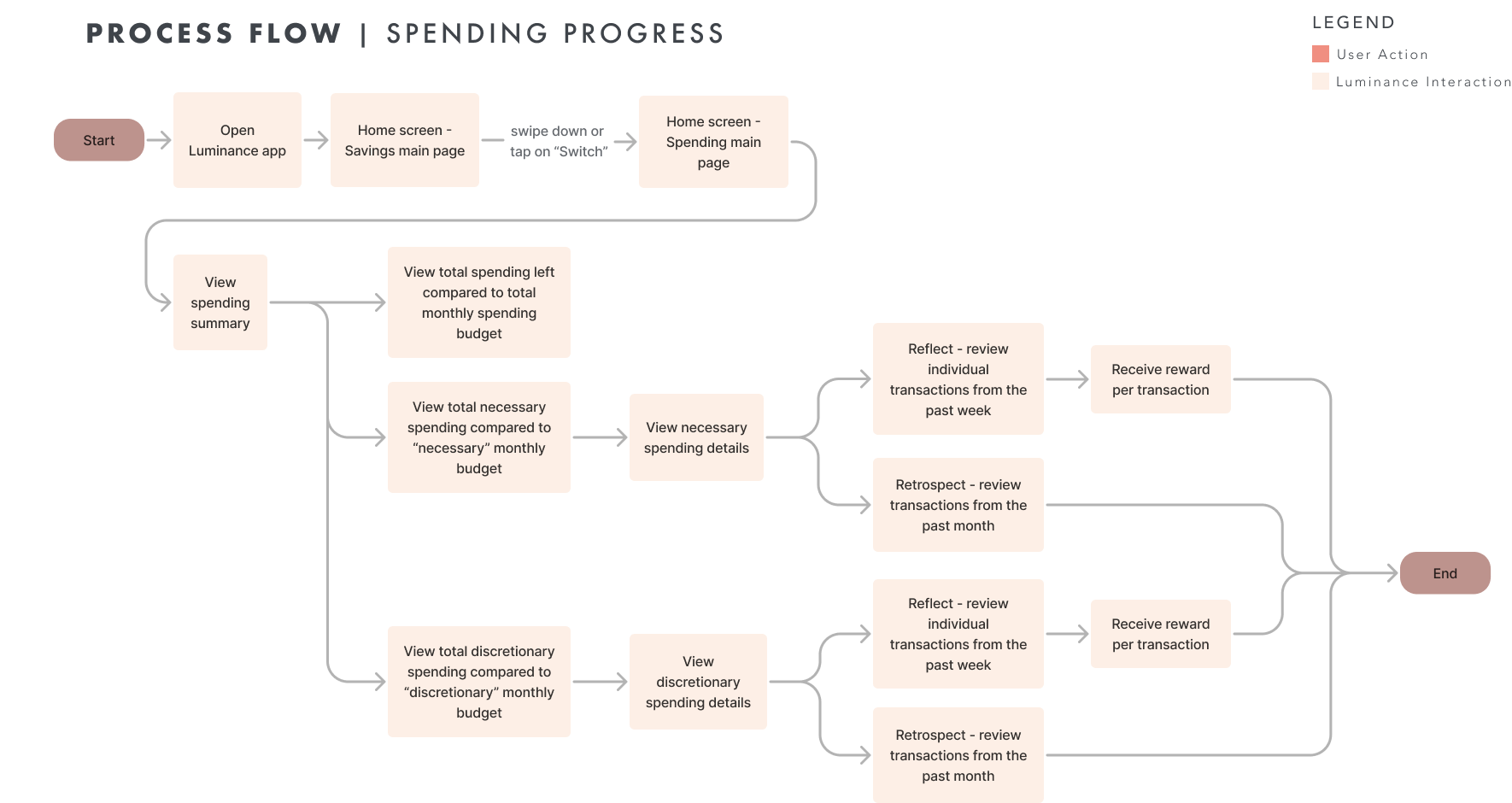

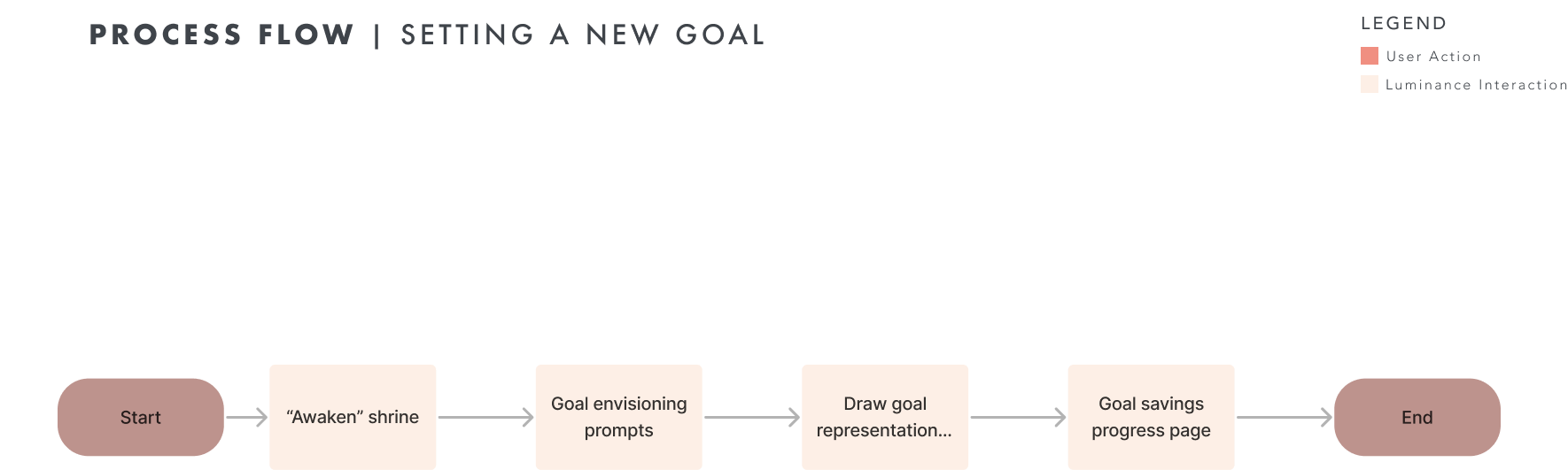

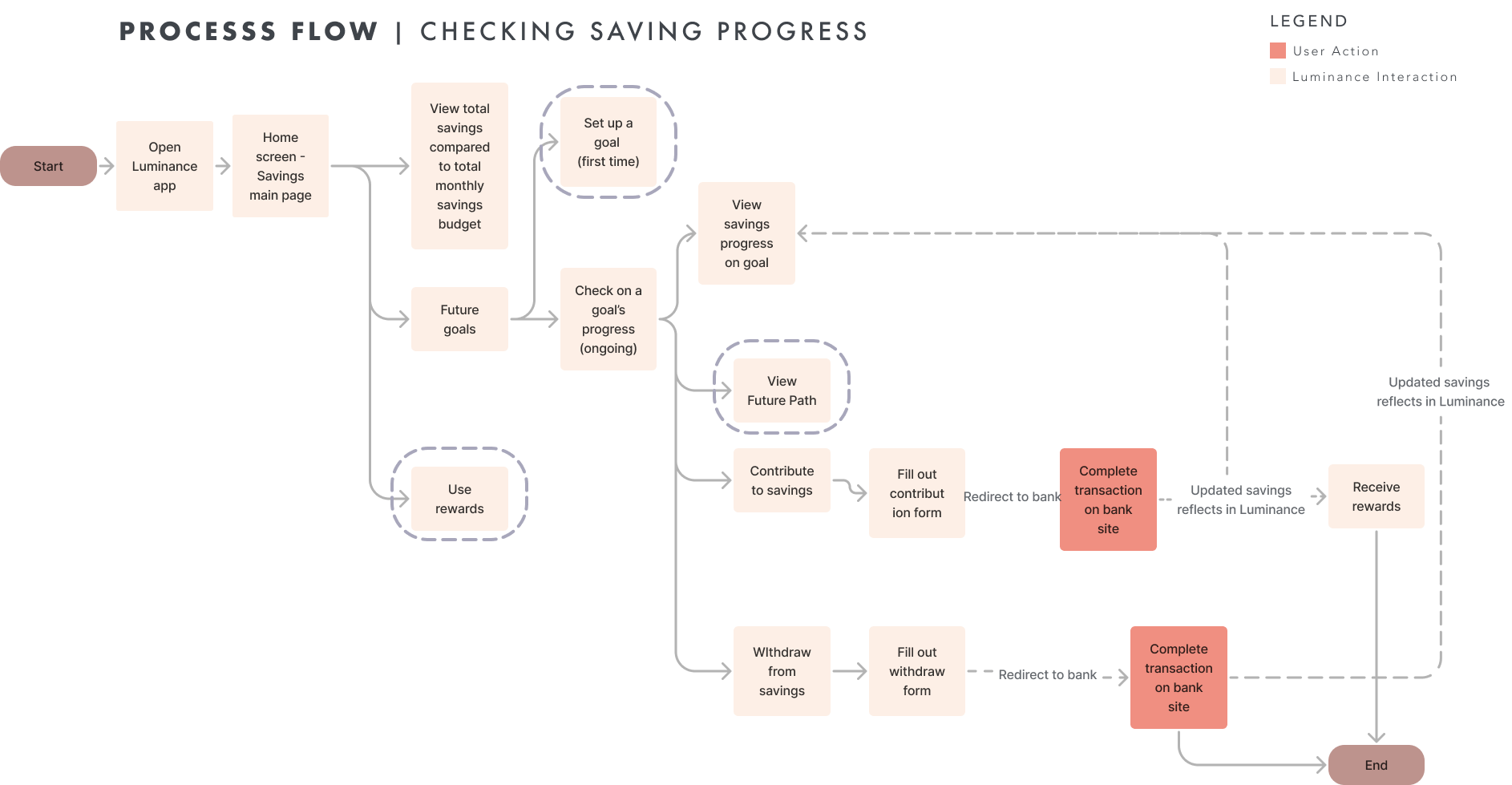

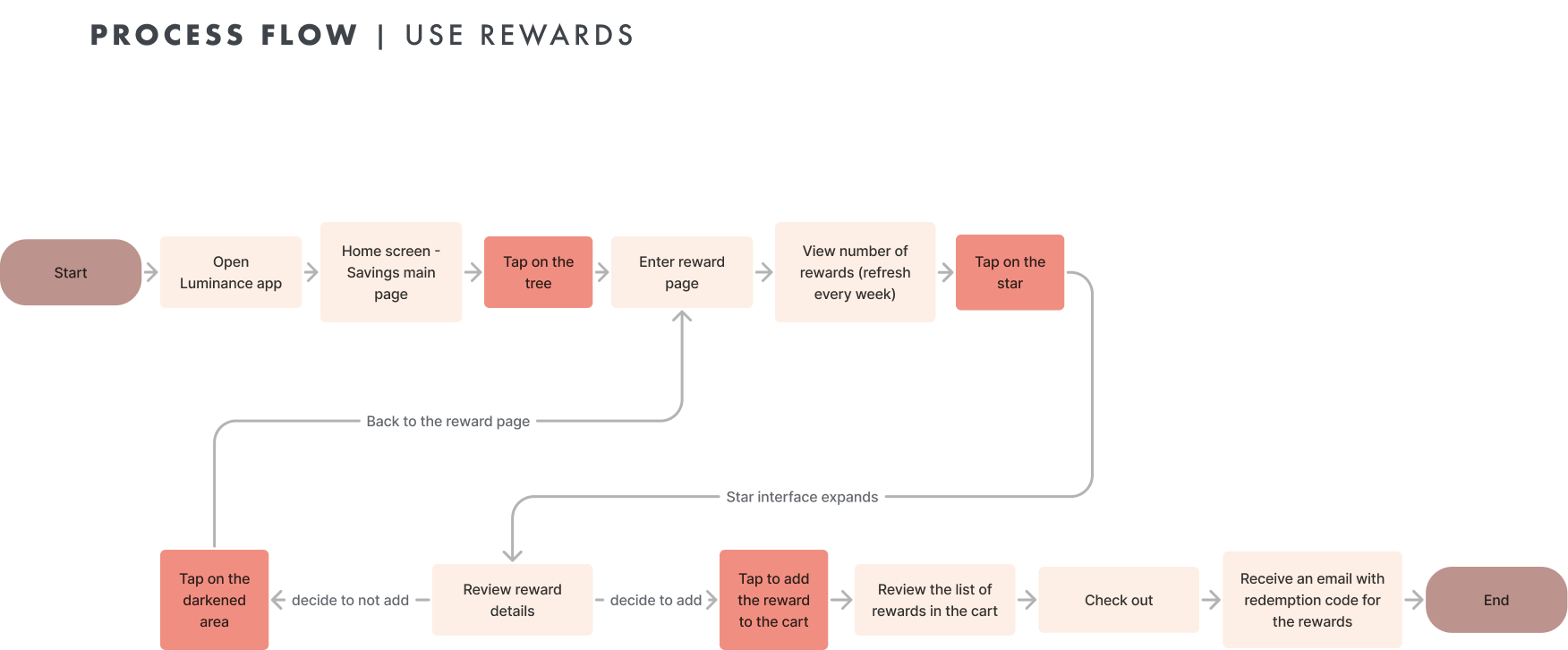

User Flow

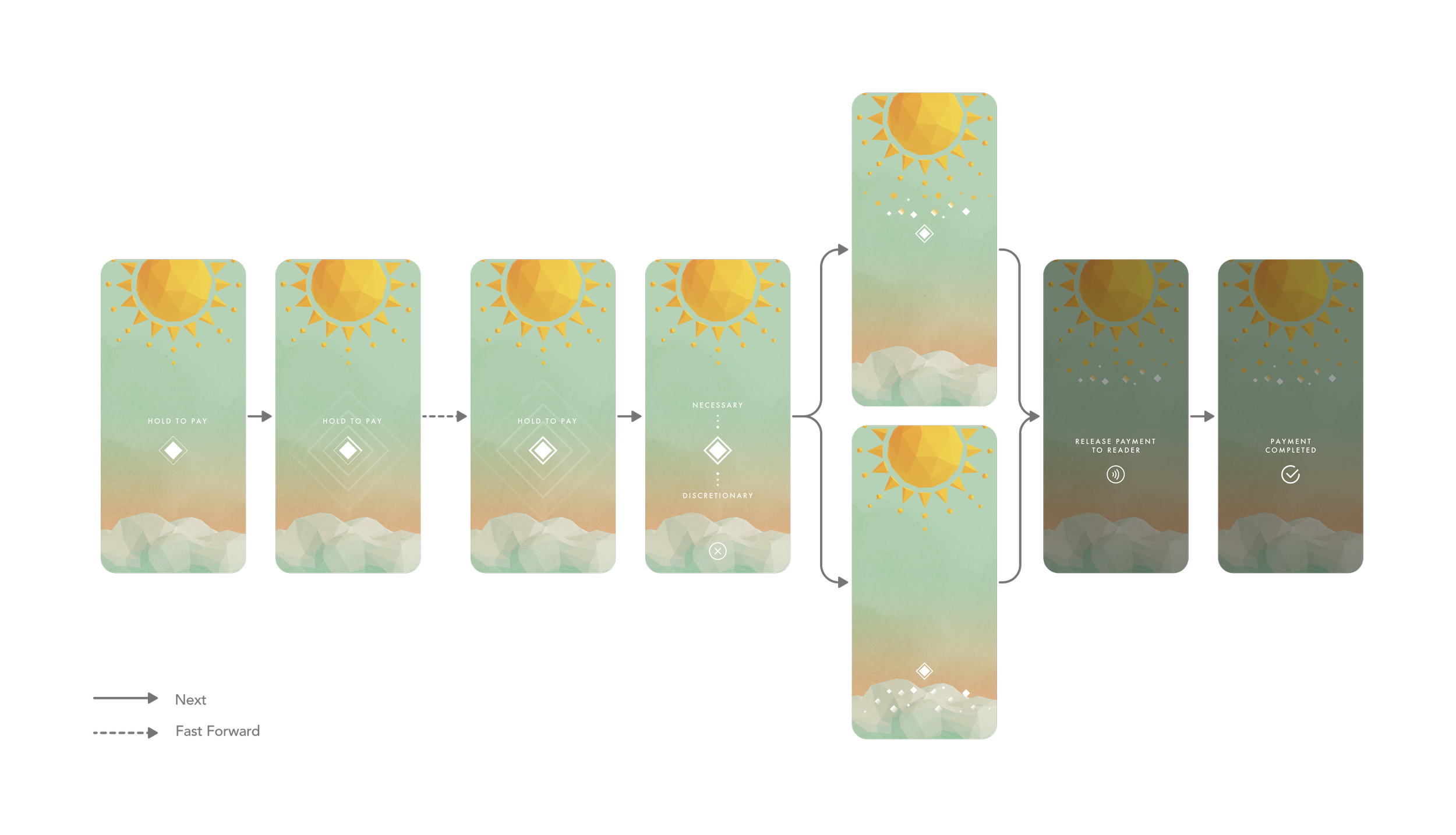

We aimed to make every interaction within the app feel intuitive and purposeful, crafting user flows that seamlessly guide users through their financial journey. Whether it's making a purchase, setting financial goals, or tracking progress, our design prioritizes a smooth and effortless experience.

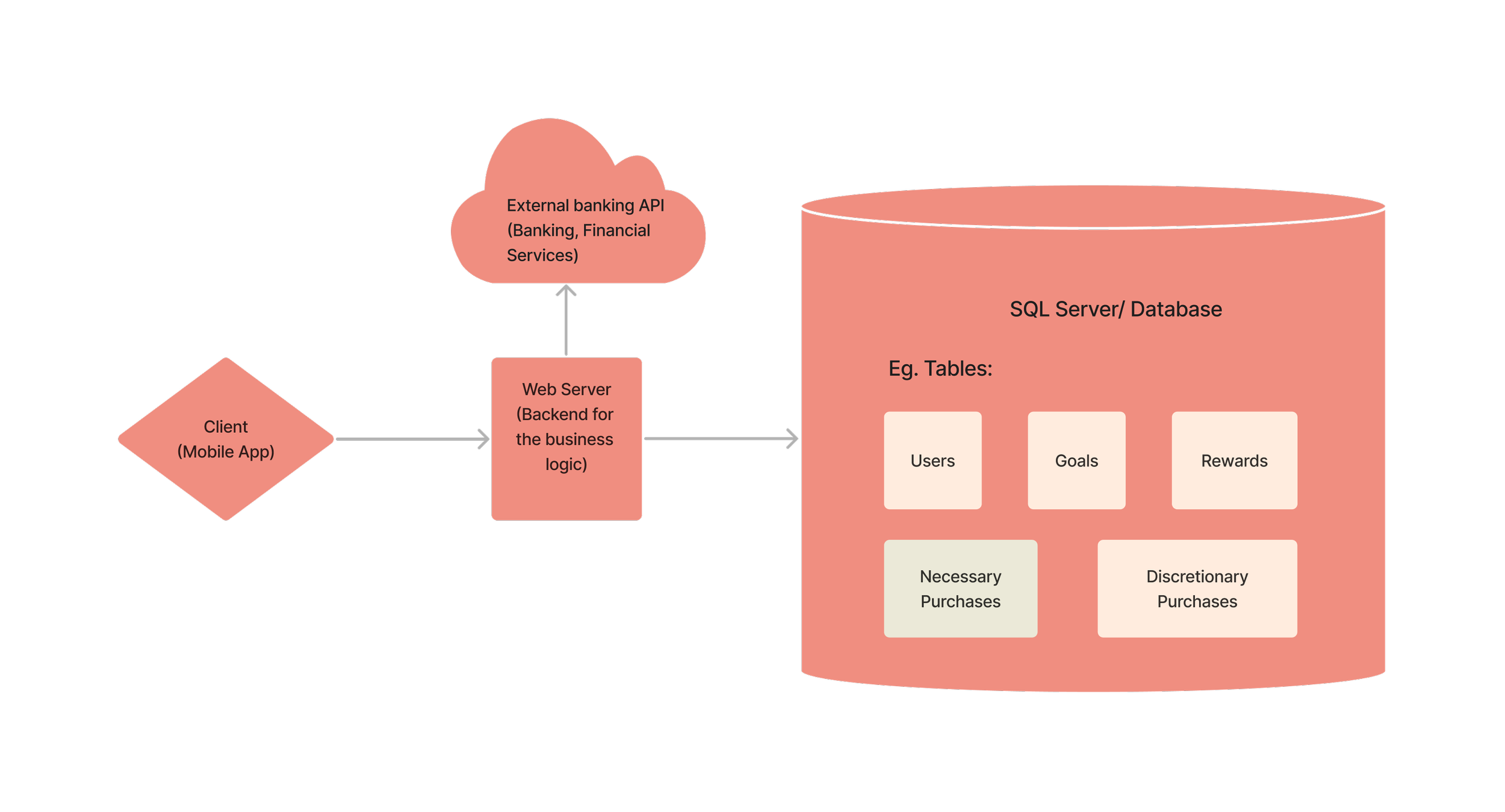

System Architecture

Luminance's system architecture is designed with user privacy and personalization in mind. As an application, users can easily create profiles and link their bank accounts.

This connection enables Luminance to offer tailored saving and spending guidance. Crucially, the app ensures the security of sensitive data by storing it in its own secure database. Luminance only accesses the necessary information from users' financial accounts, safeguarding their privacy throughout the experience.

Low-Fidelity Prototype

During the refinement of the storyboard, we simultaneously crafted the initial draft of our prototype. We incorporated some of the ideas and interactions from our initial, highly gamified concept into this early prototype.

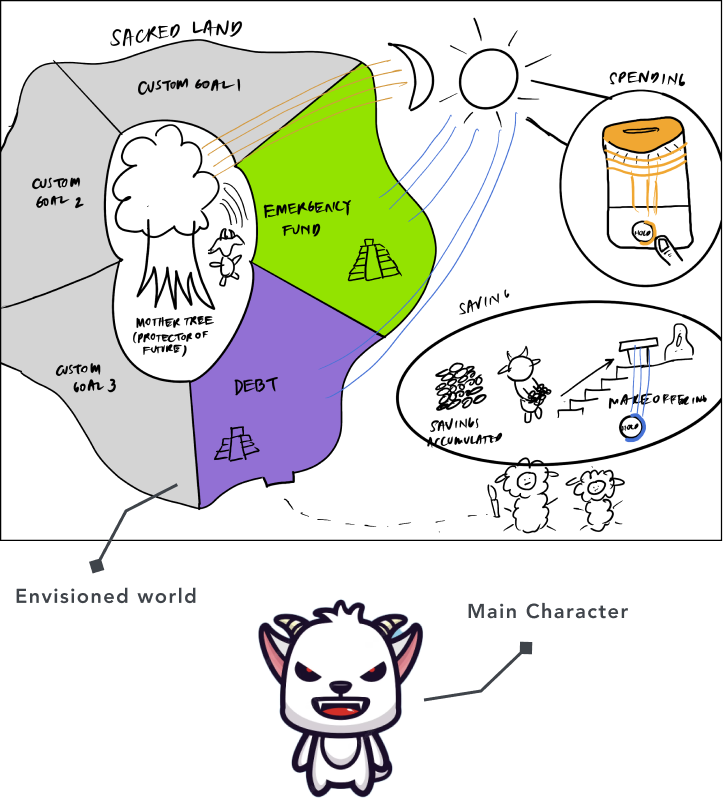

Notably, I was responsible for conceiving and developing the initial concept for the main page dedicated to savings and the innovative "Future Path." In our pursuit of balance, we aimed to seamlessly integrate these engaging gamified elements while preserving the core financial management features we were steadfastly committed to delivering.

High-Fidelity Prototype

Luminance's high-fidelity prototype represents the culmination of our dedication to providing a user-centric and engaging financial management tool with the help of intuitive features designed to simplify financial planning and empower them to make informed decisions.

Throughout this project, my central role revolved around shaping interactions on the savings page and creating functionalities that empower users to actively pursue their future financial goals. My primary task entailed translating the innovative concept of visualizing and contributing to one's financial future, symbolized by stars, into an engaging and hands-on experience.

-

To achieve this, I introduced a variety of micro-interactions and integrated multiple animations. These enhancements not only infused dynamism and fascination into the interface but also seamlessly aligned with the team's overarching vision of enabling users to effectively plan for and achieve their financial aspirations.

Aftermath

I'm committed to ongoing project improvement. I want to dig deeper into core interactions for optimization and explore expanding our platform to VR and desktop. Engaging users through testing to validate design assumptions, particularly about spending interaction, is crucial. I also aim to enhance our design system for a consistent user experience.

Reference

Image

LimeZu, L. (2020). Modern Interiors. LimeZu. Retrieved October 1, 2023, from https://limezu.itch.io/.

Rachmat, R. (2023). Evil goat mascot cartoon character design. Freepik. Retrieved October 4, 2023, from https://www.freepik.com/premium-vector/evil-goat-mascot-cartoon-character-design-premium-vector_24004156.htm.

Literature

Atchley, R. C. (1982). Retirement as a Social Institution. Annual Review of Sociology, 8(1), 263–287. https://doi.org/10.1146/annurev.so.08.080182.001403

Barroso, A. X., Parker, K., & Fry, R. (2019, October 21). More than half of young adults who receive financial help - and parents who provide help - say at least some of the help was for recurring expenses. Pew Research Center's Social & Demographic Trends Project. Retrieved April 16, 2023, from https://www.pewresearch.org/social-trends/2019/10/23/majority-of-americans-say-parents-are-doing-too-much-for-their-young-adult-children/psdt_10-23-19_youngadults-00-07/

Breitbach, E., & Walstad, W. B. (2016). Financial Literacy and Financial Behavior among Young Adults in the United States. In E. Wuttke, J. Seifried, & S. Schumann (Eds.), Economic Competence and Financial Literacy of Young Adults: Status and Challenges (1st ed., Vol. 3, pp. 81–98). Verlag Barbara Budrich. https://doi.org/10.2307/j.ctvbkk29d.7

Cachero, P. (2023, April 17). How much money do I need to retire? A quarter of Americans have no savings. Bloomberg.com. https://www.bloomberg.com/news/articles/2023-04-17/how-much-money-do-i-need-to-retire-a-quarter-of-americans-have-no-savings#xj4y7vzkg

CFI Team. (2023, March 21). Pension fund. Corporate Finance Institute. Retrieved April 16, 2023, from https://corporatefinanceinstitute.com/resources/capital-markets/pension-fund/

Curran, M.A., Parrott, E., Ahn, S.Y. et al. Young Adults’ Life Outcomes and Well-Being: Perceived Financial Socialization from Parents, the Romantic Partner, and Young Adults’ Own Financial Behaviors. J Fam Econ Iss 39, 445–456 (2018). https://doi.org/10.1007/s10834-018-9572-9

Greenwood, C. (2022, July). Young Adults Who Save for Retirement: A Grounded Theory Study of the Decision-Making Process of the Decision-Making Process. https://digitalcommons.georgefox.edu/

Kurz, C., Li, G., & Vine, D. J. (2018, November). Are millennials different? Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.C. Retrieved April 16, 2023, from https://www.federalreserve.gov/econres/feds/files/2018080pap.pdf

Lučić, A., Uzelac, M. and Previšić, A. (2021), "The power of materialism among young adults: exploring the effects of values on impulsiveness and responsible financial behavior", Young Consumers, Vol. 22 No. 2, pp. 254-271. https://doi.org/10.1108/YC-09-2020-1213

Lusardi, A. (2003, December). Planning and saving for retirement. https://static.twentyoverten.com/5df7ffacb22b20786b33bcac/6YoHI1IFiT/Lusardi_pdf.pdf

Lusardi, A., & Mitchell, O. (2011). Financial literacy and retirement planning in the United States. Journal of Pension Economics & Finance, 10(4), 509-525. doi:10.1017/S147474721100045X

Melissa, K. A. Z. (2012, January 11). I Do … Want to Save: Marriage and Retirement Savings in Young Households. Wiley Online Library. Retrieved April 16, 2023, from https://onlinelibrary.wiley.com/doi/10.1111/j.1741-3737.2011.00877.x

Meyers, E. (2020). Young Adult Financial Literacy and Its Underlying Factors. Retrieved April 16, 2023, from https://digitalcommons.assumption.edu/cgi/viewcontent.cgi?article=1063&context=honorstheses

Mustafa, W. M. W., Islam, M. A., Asyraf, M., Hassan, M. S., Royhan, P., & Rahman, S. (2023). The Effects of Financial Attitudes, Financial Literacy and Health Literacy on Sustainable Financial Retirement Planning: The Moderating Role of the Financial Advisor. Sustainability (Basel, Switzerland), 15(3), 2677–. https://doi.org/10.3390/su15032677

Ntalianis, Michael and Wise, Victoria, The Role of Financial Education in Retirement Planning, Australasian Accounting, Business and Finance Journal, 5(2), 2011, 23-37.

Philippot, C. M. (2020). A Bit Pricey: Young Adults’ Financial Literacy, Financial Decision-Making Process, and Spending Habits (thesis).

Rhee, N. (n.d.). Conquering the seven faces of risk. Conquering the Seven Faces of Risk. Retrieved April 16, 2023, from https://www.sumgrowth.com/FinTechPress/Conquering-the-Seven-Faces-of-Risk.aspx

Semuels, A. (2020, January 15). This is what life without retirement savings looks like. The Atlantic. https://www.theatlantic.com/business/archive/2018/02/pensions-safety-net-california/553970/